European telecom operators are investing heavily in 5G, fibre, AI, and network modernisation. Yet despite this sustained investment, financial performance across the sector remains under pressure.

Revenue growth is modest, margins are tightening, and returns on capital are declining. This raises an important question: why aren't these investments translating into stronger outcomes?

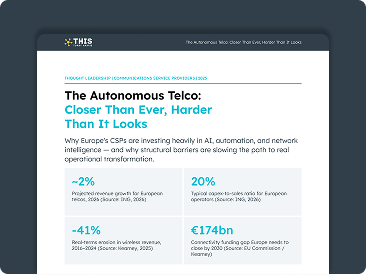

The paradox: Rising investment, weak returns

At a headline level, the European telecom sector appears relatively stable, with projected revenue growth of around 2% in 2026.

However, a closer look reveals deeper structural challenges.

Capex intensity continues to hover at approximately 20% of revenues, driven by ongoing investments in 5G standalone networks, fibre infrastructure, and AI capabilities. At the same time, the value of connectivity has declined significantly in real terms, with wireless revenues eroding by roughly 41% over the past decade.

Operators are caught in a difficult position, required to invest continuously just to remain competitive, without seeing proportional financial returns.

The cost of staying relevant

Over the past few years, telecom operators have made genuine progress in improving efficiency. Automation has reduced manual workloads, AI is enhancing customer service and network operations, and virtualisation has increased flexibility.

Yet these efficiency gains are being offset by the cost of keeping up with industry demands.

Continuous infrastructure upgrades, AI platform investments, and organisational restructuring are absorbing much of the value generated. In effect, operators are running faster, but not necessarily moving ahead.

AI adoption without scaled impact

AI is often positioned as the solution to both cost pressures and operational complexity. Adoption across the industry is strong, with most operators actively investing in AI-driven use cases.

However, many of these initiatives remain confined to pilot phases or limited deployments. The challenge is not a lack of ambition or funding, but an inability to scale AI effectively across the organisation.

This is largely due to underlying structural constraints:

- Fragmented and inconsistent data environments

- Legacy OSS/BSS systems that are not designed for real-time, API-driven operations

- Gaps in governance and business ownership

As a result, AI is being implemented, but not fully operationalised.

The Hidden bottleneck: Integration and architecture

The root cause behind many of these challenges lies in how systems, data, and processes are connected.

Many telecom environments today are characterised by siloed data across OSS, BSS, and network layers, along with point-to-point integrations and rigid, monolithic architectures. These limitations create complexity, slow down innovation, and restrict the ability to scale new capabilities.

Without a cohesive integration layer, every new investment adds another layer of complexity rather than unlocking new value.

Shifting focus: Building the right foundation

Operators that are making measurable progress are not simply increasing investment, they are focusing on strengthening foundational capabilities.

This includes:

- Moving towards composable, API-led architectures

- Establishing unified and governed data platforms

- Enabling intelligent orchestration across domains

- Building seamless integration with ecosystem partners

These capabilities create the conditions required for AI, automation, and network innovation to deliver tangible business outcomes.

What this means for technology leaders

For CIOs and technology leaders, the strategic question is no longer whether to invest in AI or next-generation networks.

The focus must shift to whether the organisation has the right foundation to extract value from these investments.

Key considerations include:

- Whether AI systems can access consistent, real-time data across domains

- Whether there is a governed API layer enabling scalable integrations

- Whether the current architecture can evolve without significant disruption

Without these foundations, additional investment risks increasing complexity rather than improving performance.

Conclusion

European telcos are not under-investing. The challenge lies in how effectively that investment is translated into value.

The gap between spending and outcomes is driven less by technology limitations and more by structural and architectural constraints.

Closing this gap requires a shift in focus, from investing in new technologies to building the integration, data, and architectural foundations that allow those technologies to deliver at scale.

For deeper insights on this topic, download the full report

Frequently asked questions

European telcos are struggling because increased investment in 5G, fibre, and AI is not translating into proportional returns. Structural challenges such as legacy systems, fragmented data, and integration complexity limit the ability to scale new technologies effectively.

One of the biggest European telcos challenges is the gap between investment and outcomes. While operators are investing heavily in infrastructure and AI, they lack the architectural and integration foundations needed to unlock value at scale.

European telecom revenue growth remains modest due to declining value of connectivity, high competition, and price pressures. Even as usage increases, real-term revenues have fallen, especially in wireless services.

Margins are declining because of high capital expenditure (around 20% of revenue), continuous network upgrades, and increasing operational costs. Efficiency gains from automation and AI are often offset by these ongoing investments.

AI is helping telecom operators improve customer service, automate operations, and optimize networks. However, many AI initiatives are still in pilot stages and not fully scaled due to data, integration, and governance challenges.

|

Pankaj KulkarniSenior Manager Research & InisghtsTorry Harris Integration Solutions |